General Enquiries:office@whlaw.com.au

Perth:+61 8 9481 2040

Geraldton:+61 8 9921 2344

Employee versus contractor? Are you sure?

Over the past decade many Australian companies have retained the services of people who claim they are "contractors" not employees. Usually the "contractor" wants to be paid a gross fee/remuneration, stating that they will take care of income tax, superannuation and other payments.

The attraction for the employer is a lower total cost of retaining the person as compared to bringing them on as an employee, as well as perceived flexibility in options for ending the relationship as compared to traditional employment (the thinking is that no redundancy or leave entitlements need to be paid and no notice period applies).

Such practices were common in the IT, marketing, construction and other industries, particularly so called “digital industries”. The “gig economy” has seen the practice gain pace.

The legal reality is that many "contractors" are actually employees, particularly where they turn up to work at the same place each day, take their instructions from "a boss" at the company, are paid by the hour rather than for delivering an end product, and don't have to redo their work at their cost if the deliverable is not done to the required standard.

In such cases, income tax and compulsory superannuation guarantee payments must be paid by the employer for "contractors" who are, legally, employees. If the payments are not made, significant penalties accrue over time and must be paid to the Australian Tax Office (ATO).

Often this superannuation liability only hits home when the employer tries to sell their company and the buyer's due diligence experts point out the problem. Significant superannuation shortfall payments and ATO penalties loom large for the seller, as well as a reduction in the sale price, or at least a significant escrow sum demanded by the buyer.

A superannuation guarantee amnesty is potentially available.

Legislation has been reintroduced to Parliament providing an amnesty for employers who have not paid superannuation guarantee (SG) payments. The proposed amnesty will allow fines to be avoided, provided the SG payments are made.

The Treasury Laws Amendment (Recovering Unpaid Superannuation) Bill 2019 (the Bill) was re-introduced into the House of Representatives on 18 September 2019. The Bill was then referred to the Economics Legislation Committee for further inquiry. The Committee released its report recently - available here.

The Bill provides employers who have previously failed to pay SG contributions and failed to disclose the shortfall to the ATO with a “second chance” to self-correct any historical non-compliance.

This amnesty operates as a way for the ATO to encourage employers to disclose unpaid SG amounts for the period during which the amnesty applies - without fear that they will be liable for fines typically associated with non-compliance.

What are my SG obligations generally?

The Superannuation Guarantee (Administration) Act 1992 (SGAA) requires that employers pay a certain percentage of an employee’s earning into the employee’s superannuation fund. A Superannuation Guarantee Charge (SGC) is imposed on employers who fail to pay the required SG amount i.e. the SGC is the shortfall plus interest and administration costs, and this is payable by the employer to the ATO each quarter.

Employers can also be liable for penalties for failing or refusing to provide a statement or information as required under the SGAA, which can be up to 200% of the amount of the underlying SG amount (known as Part 7 Penalties).

How will the proposed amnesty work?

The first step is disclosing unpaid SG to the ATO. An employer who discloses SG non-compliance and pays an employee’s full SG entitlements plus any interest (which may incude nominal interest and a general interest charge (GIC)) will be entitled to the amnesty, and will avoid liability for penalties normally associated with late payment and non-compliance.

The employer with an outstanding SG liability can either:

However, if employers have an existing SGC assessment for a quarter, or are otherwise unable to contribute directly into their employee’s superannuation fund, they will be required to pay the SGC to the Commissioner directly.

If the employer makes a disclosure under the amnesty, the administration charge component of the SGC will be waived (see example 1.1 in the Explanatory Memorandum).

The amnesty is proposed to extend to all reporting quarters from the quarter commencing 1 July 1992 to the quarter commencing 1 January 2018.

The disclosure to the ATO must be made in the correct form, and the employer must pay the amount of the disclosed SG to the employee or the SGC to the ATO (see above) within the required period. Failure to pay will mean the employer will not be able to rely on the amnesty and will be subject to the normal penalties imposed.

It is expected that employers will be given from 24 May 2018 to 6 months after the date the Bill receives Royal Assent to make disclosure and pay the shortfall and interest (the Amnesty Period).

In summary, in order to benefit from the amnesty the unpaid SGC must:

The employer must also:

If the employer does the above things for eligible SG shortfalls, they will not be liable for Part 7 Penalties. SG amounts paid during the Amnesty Period will be tax deductable.

If the Bill is passed, employers who have failed to comply with their SG obligations in the past should take advantage of this opportunity to avoid liability for such penalties.

Employers who fail to disclose during the Amnesty Period

Employers who do not disclose and pay unpaid SG and interest within the Amnesty Period will be subject to higher penalties. Generally, the Commissioner has discretion to remit Part 7 Penalties. However, from the day after the Amnesty Period ends the Commissioner’s ability to remit Part 7 Penalties will be limited. According to the Explanatory Memorandum, the Commissioner will not be able to remit penalties below 100% of the amount of SGC owing by the employer for a quarter covered by the amnesty. The penalty will include interest and an administration fee.

What does this mean for my business?

The amnesty is a one-off second chance for employers to reduce their exposure to penalites for unpaid SG. Employers who are aware that they have failed to comply with their SGC obligations, or are unsure whether they have fully complied since 1 July 1992, should ensure that they keep informed of the progress of the Bill.

In particular, employers who have utilised the services of “contractors” who look-and-feel like employees should consider taking advice on whether the persons involved were legally employees for the purposes of tax, superannuation and other legislation.

If you would like further information regarding the new laws or any other issue please contact Damian Quail or Cassandra Bailey.

This article is general information only, at the date it is posted. It is not, and should not be relied upon as, legal advice. This article might not be updated over time and therefore may not reflect changes to the law. Please feel free to contact us for legal advice that is specific to your situation.

It is not uncommon for businesses to advertise a headline price for goods and services to their customers, and to only disclose optional costs in the fine print or in a manner that is not necessarily clear to customers. This is no longer permitted. Some businessess will need to change their pricing practices, particularly businesses selling goods online.

The Treasury Laws Amendment (Australian Consumer Law Review) Bill 2018 amends the Australian Consumer Law contained within the Competition and Consumer Act 2010, and imposes an obligation on businesses operating in Australia to ensure transparent pricing for consumers. As of 26 October 2019, businesses must display the total price for the goods and services including all pre-selected optional items. In other words, if optional components are pre-selected or automatically applied by the seller, these options must be included in the headline price. The customer then has the option to remove the pre-selected options selected in order to pay a lower price.

These new laws will especially affect businesses who sell goods and services online. The Explanatory Memorandum to the new legislation provides some helpful examples in relation to airlines. For example, if an airline fare is $500 and a website pre-selects an optional carbon offset fee of $5, then the headline price must be $505, not $500. However, if the carbon offset fee is not pre-selected or automatically applied, then the ticket can be advertised at $500.

The same approach is applicable for promotions which display only a portion of the total price. Businesses must ensure that the total price is displayed just as clearly as the fractional price. Essentially, the new laws aim to avoid the situation where headline prices are advertised initially, but once the customer clicks through the website the price is increased to include pre-selected options and charges.

Businesses should ensure that their pricing strategies conform with the new laws.

If you would like further information regarding the new laws please contact Damian Quail.

This article is general information only, at the date it is posted. It is not, and should not be relied upon as, legal advice. This article might not be updated over time and therefore may not reflect changes to the law. Please feel free to contact us for legal advice that is specific to your situation.

Modern slavery legislation has been enacted in Australia. Many larger companies are now legally obliged to prepare Modern Slavery Statements and submit these statements to the Australian Federal Government. The Statements will be published on a publicly accessible register.

At its broadest, the term "modern slavery" refers to any situations of exploitation where a person cannot refuse or leave work because of threats, violence, coercion, abuse of power or deception. It encompasses slavery, servitude, deprivation of liberty, the worst forms of child labour, forced labour, human trafficking, debt bondage, slavery like practices, forced marriage and deceptive recruiting for labour or services. Indicators of modern slavery practices may incude unlawful withholding of wages and identity/travel documents through to excessive work hours and restrictions on movement. Other indicators include recruitment agencies deducting excessive fees from worker remuneration, loans to workers with astronomical interest, and similar practices.

The Walk Free Foundation, which publishes the annual Global Slavery Index, estimates that 30.4 million people are victims of modern slavery in the Asia Pacific region, including within Australia (Walk Free Foundation, Global Slavery Index 2016, www.globalslaveryindex.org). Many Australian companies source workers, products and services from the Asia Pacific region.

For many of these larger companies, reports will need to be lodged between 1 July 2020 and 31 December 2020. It is crucial that affected companies begin reviewing their internal processes and supply chains and begin collecting data to comply with the new reporting obligations.

What does the Federal legislation require?

The Federal legislation is the Modern Slavery Act 2018 (Cth). It commenced on 1 January 2019.

Key aspects of the Federal legislation are as follows:

No penalties exist in the legislation for not complying with the Act. However, the Government has indicated that if compliance rates are low, the need for penalties will be considered as part of a three year review of the legislation.

Many prominent Australian companies such as Wesfarmers, South 32, Qantas and Fortescue Metals have already published Modern Slavery Statements.

What does the New South Wales legislation require?

The NSW legislation - the Modern Slavery Act 2018 (NSW) - is not yet in force. It was assented to on 27 June 2018, but it has not yet commenced operation. On 6 August 2019 the NSW Legislative Council Standing Committee on Social Issues announced an inquiry into the NSW Act. The Committee's recommendations are due on 14 February 2020.

Key aspects of the proposed NSW Act are as follows:

It is not yet certain whether the NSW legislation will operate in addition to the Federal legislation, or whether it will only operate when the Federal legislation does not apply to a particular company. The proposed NSW Act states that the reporting requirements under the NSW Act will not apply if the organisation is subject to obligations under a law of the Commonwealth or another State or a Territory. So, a possilbe outcome is that companies that file a Modern Slavery Statement under the Federal legislation will not need to report under the NSW Act as well. However, companies operating in NSW with revenue between $50 and $100 million may need to comply with the NSW Act once it commences operation, as they will be caught by the NSW Act but not the Federal Act.

What does the Western Australian legislation require?

Nothing yet- Western Australia has not yet enacted its own Modern Slavery legislation. However, it seems inevitable that Western Australian legislation will arrive at some point.

Next steps

It is crucial that companies required to report under the Modern Slavery Legislation begin reviewing their internal processes and supply chains and begin collecting data to comply with the new reporting obligations. This could include:

For further information on managing your risk and compliance obligations, please contact Damian Quail.

This article is general information only, at the date it is posted. It is not, and should not be relied upon as, legal advice. This article might not be updated over time and therefore may not reflect changes to the law. Please feel free to contact us for legal advice that is specific to your situation.

The importance of minute taking at Board meetings was recently highlighted by the Financial Services Royal Commission. The Governance Institute of Australia and the Australian Institute of Company Directors have collaborated to publish a Joint Statement of Board Minues (Joint Statement, available on the AICD’s and the Governance Institute's websites), which outlines key principles and best practice approaches to minute taking and document retention.

In many ways, the Joint Statement provides a “best practice” guideline for recording decisions and discussions at Board meetings. Company officeholders would be wise to carefully review the Joint Statement and ensure they are adequately recording minutes of Board meetings and complying with their statutory obligations. We have summarised below five key takeaways from the Joint Statement.

1. Board minutes are a legal record

Board minutes are a legal record of Board decisions. The minutes may be the best, and sometimes only, evidence of the decision making process at Board meetings. Minutes may help to establish that directors have satisfactorily exercised their powers and discharged their duties.

Minutes should include the key points of discussion and detail the issues and risks the Board has considered. If judgment is required and directors are balancing a number of competing risks, it is prudent to consider whether the minutes capture them adequately. This is important where directors wish to rely on the “business judgement rule”.

2. Balance the level of detail

The Joint Statement highlights the importance of ensuring the information recorded contains a sufficient level of detail. Too much information can be unhelpful and too little can cause ambiguity. The right balance needs to be struck.

In summary, Board minutes should record:

However, Board minutes should not record:

The Board paper and supporting documentation used in the decision making process should influence the details in the minutes. Where appropriate, minutes should refer to the Board paper and supporting documents, but avoid repeating the contents. In that regard, directors should take an active role in reviewing Board papers and satisfying themselves that they provide adequate information on which to base decisions.

3. Stick to a particular style

The Joint Statement provides some helpful stylistic tips for drafting minutes, including that minutes should:

4. Consider regulatory and statutory compliance

It is a requirement of the Corporations Act 2001 that a company keep a minutes book in which proceedings and decisions at Board meetings are recorded within one month of the meeting. It is important directors understand the statutory obligation - failing to do so is an offence of strict liability.

Minutes must be signed by the chair of the meeting, or by the chair of the next meeting, within a reasonable time after the meeting takes place. All directors should be given an opportunity to review and discuss the minutes before they are approved and signed.

Companies should implement (or review their current) document retention policies. It may be necessary to seek legal advice regarding what policies should be implemented and the obligations to safeguard evidence.

5. Be wary of Legal Professional Privilege

It is common for Boards to consider legal advice. A cautionary approach should be taken in determining the degree of privileged information to include in the minutes. In many cases, it may be sufficient to document that the Board considered relevant legal advice when making a particular decision. Any privileged information in the minutes should be clearly identified and ideally be included in an appendix. Importantly, where minutes refer to privileged advice they should not be provided to third parties without first obtaining legal advice as this may waive privilege.

If you require further advice about conducting Board meetings or corporate governance or advice generally, please do not hesitate to contact Cassandra Bailey at cassandra.bailey@whlaw.com.au or 9481 2040.

This article is general information only, at the date it is posted. It is not, and should not be relied upon as, legal advice. This article might not be updated over time and therefore may not reflect changes to the law. Please feel free to contact us for legal advice that is specific to your situation.

The interaction between section 249D and section 203D of the Corporations Act 2001.

There has been a significant rise in shareholder activism over the last couple of years. Often this is driven by shareholders with financial capacity and vision for the company, wanting to turn around the company’s stagnant fortunes and share price. A common mechanism for shareholders to replace the board of a public company is a section 249D notice under the Corporations Act 2001. A section 249D notice allows a shareholder or shareholders with at least 5% of a company’s share capital to force the company to call a general meeting to vote on resolutions proposed in the notice.

There are a number of formal requirements, and many tricks and traps for shareholders, in utilising the section 249D notice provisions.

The section 249D notice must be in writing, state any resolution to be proposed at the meeting, be signed by the members making the request, and be given to the company.

On receipt by the company of a valid section 249D notice:

If the section 249D notice proposes resolutions for the removal of all or certain directors, the requirements of section 203D Corporations Act 2001 also need to be kept in mind. Section 203D(2) requires shareholders who want to remove a director at a general meeting, to give notice of their intention at least 2 months before the meeting is to be held. The second part of section 203D(2) provides that if the company calls a meeting after that notice of intention is given, the director can be removed at the meeting even if the meeting is held less than 2 months after the notice of intention is given.

It is the structure of section 203D and the interplay between sections 203D and 249D that tends to cause grief for requisitioning shareholders.

Common mistakes

Because section 249D does not explicitly refer to section 203D it is sometimes overlooked. If a section 203D notice has not been given, or it is given after the section 249D notice, a proposed resolution in the section 249D notice to remove a director is ineffective and there would be a question whether the company had to call the meeting at all.

Other issues we sometimes see are the two notices being combined into one, or being issued on the same day.

The two notices cannot be combined. That is, the section 249D notice cannot also serve as the shareholder giving notice of their intention under section 203D. There are at least a couple of reasons for this.

As well as being separate notices, the section 203D notice should be given to the company before the section 249D notice is delivered; not on the same day. That is the only way sections 203D and 249D can operate harmoniously and with full effect.

The section 203D notice can and should be given in such a way that it is possible for the meeting to be held after the 2 month period required by section 203D (although the company may then make its own decision to bring the meeting forward as foreshadowed by the second part of section 203D). This can only happen if the section 249D notice is given to the company at least a day after the section 203D notice is given; preferably longer (out of an abundance of caution). The exact timing will depend on the circumstances in each case.

We recommend that shareholders intending to use section 249D to remove directors from the board of a public company get legal advice on the process, and assistance to ensure each step is properly planned and executed. Conversely, directors receiving such notices should seek prompt advice about how to manage their obligations under the Corporations Act 2001 and what steps can be taken to defend themselves and the company against the attack.

For advice to prepare for or defend an attempted board spill, please contact Dominique Engelter on +61 9481 2040 or dominique.engelter@whlaw.com.au.

This article is general information only, at the date it is posted. It is not, and should not be relied upon as, legal advice. This article might not be updated over time and therefore may not reflect changes to the law. Please feel free to contact us for legal advice that is specific to your situation.

Uber Eats agreed this week to amend its contracts with restaurants following an investigation by the ACCC.

From at least 2016, Uber Eats’ contracts made restaurants responsible for the delivery of food orders despite the restaurants having no control over delivery. Under the contracts, if food became “substandard” (for example hot food became cold), Uber Eats could force restaurants to refund the costs of the food to customers, regardless of whether the issue was the restaurants fault.

ACCC chair Rod Sims said that the ACCC considers these terms to be unfair “because they appear to cause a significant imbalance between restaurants and Uber Eats; the terms were not reasonably necessary to protect Uber Eats and could cause detriment to restaurants."

Uber Eats agreed to amend these terms to make it clear that restaurants will only be responsible for matters within their control, such as incorrect food items or incorrect and missing orders. Under the amended contracts, restaurants will also be given the ability to dispute responsibility for refunds to customers and Uber Eats will reasonably consider these disputes.

Mr Sims said that the case was a “great illustration” of why the Australian Consumer Law (ACL) needs to change. Under the current ACL, a court can declare unfair contract terms to be void and unenforceable, but they are not illegal and penalties cannot be imposed. Mr Sims said that if such contracts were illegal, “we’d be taking them to court for significant penalties.”

Red Rich Fruits

The agreement from Uber follows on from the case involving Red Rich Fruits, a fresh fruit trader, agreeing to amend its standard form contract with growers last month after the ACCC raised concerns that the contract contained an unfair contract term.

The contract term in question allowed Red Rich Fruits to seek credit from a grower in respect of produce which Red Rich Fruits had on-sold to a third party, but which was rejected by the third party. The ACCC considered it likely that this term was an unfair contract term in breach of the ACL. The ACCC also raised concerns that Red Rich Fruits’ standard form contract included terms that did not comply with the pricing formula and payment transparency terms set out in the Horticulture Code of Conduct, a mandatory industry code prescribed under the Competition and Consumer Act 2010.

Red Rich Fruits agreed to amend the pricing and payment clauses in its standard form contract in response to the ACCC’s concerns.

What does this mean for your business?

These cases demonstrate the ACCC’s willingness to crack down on the use of unfair contract terms by businesses across all industries.

The ACCC has also indicated that strengthening unfair contract term protections for small businesses remains one of its top priorities. The ACCC has called for legislative changes so that it can seek penalties and compensation for small businesses where large businesses impose unfair terms.

To avoid sanction by the ACCC and bad publicity (and possible penalties in the future), all businesses should review their standard form contracts to determine if any terms are unfair.

For further information on unfair contract terms and how we can assist you please contact, please contact Damian Quail or Hanna Forrest on +61 8 9481 2040 or damian.quail@whlaw.com.au or hanna.forrest@whlaw.com.au.

This article is general information only, at the date it is posted. It is not, and should not be relied upon as, legal advice. This article might not be updated over time and therefore may not reflect changes to the law. Please feel free to contact us for legal advice that is specific to your situation.

Background

Jump Swim is an Australian-based franchisor that sells franchises to franchisees wishing to operate their own Jump Swim School to supply learn-to-swim services to children. According to its website Jump Swim has over 65 swim school locations in Australia, and has established operations in Brazil, New Zealand and Singapore.

ACCC secures freezing order against Jump Swim

On 7 June 2019 Justice O’Bryan of the Federal Court made orders freezing the assets of Jump Loops Pty Ltd (Jump Loops) and its parent company Swim Loops Holdings Pty Ltd (collectively Jump Swim), various associated entities of Jump Swim and Jump Swim’s managing director, Ian Campbell. His Honour also ordered that Jump Swim and the associated entities identify their liquid assets world-wide comprising cash securities and deposits of any kind held with a financial institution.

Why is the ACCC taking action?

The ACCC instituted proceedings against franchisor Jump Swim in the Federal Court, alleging that it made false, misleading or deceptive statements about Jump Swim School franchises, in breach of the Australian Consumer Law (the ACL). The freezing order was sought prior to commencing the misleading and deceptive conduct action, for reasons as explained below.

The ACCC is alleging that Jump Swim made representations in its promotional material that a prospective Jump Swim School franchisee would have an operational swim school within 12 months of signing a franchise agreement, when it did not have reasonable grounds for making that statement.

The ACCC claims that there are over 90 Jump Swim franchisees who did not receive an operational swim school within 12 months or at all. The initial costs of setting up a Jump Swim School generally ranged from approximately $150,000 to $175,000.

What is a freezing order?

A freezing order is a form of injunction restraining a party from parting or dealing with property prior to a final court judgment.

The purpose of a freezing order is to prevent the frustration or inhibition of the Court’s process by seeking to avoid the danger that a judgment or prospective judgment of the Court will be wholly or partly unsatisfied because assets have been dissipated.

The principles for granting a freezing order are well established:

The Court’s judgement on the freezing order application

In regards to the first condition, Justice O’Bryan was satisfied that the evidence produced by the ACCC shows that there was at least a serious question to the tried whether the alleged conduct of Jump Swim amounted to contraventions of the ACL. This appeared to include conduct that the franchises were sold on a ‘turn-key’ basis, to be handed over and ready to operate and, a representation in the promotional material that there would be a “12 month turnaround from sign to open” of the franchise. The Court referred to the ACCC’s claim that representations made were false, misleading or deceptive and/or likely to mislead or deceive because some 90 franchisees were not provided with an operational franchise within 12 months.

As to the second condition, His Honour was also satisfied that there was a reasonable apprehension that assets owned directly or indirectly by Jump Swim and Mr Campbell would be dissipated so as to frustrate the relief sought by the ACCC. This apprehension arose from the fact that Mr Campbell and Jump Swim were facing multiple proceedings in Australia, new corporate entities had been recently created to acquire and take over the franchise business and Mr Campbell had established similar business operations in America and New Zealand (and there was evidence of material financial transactions between the Jump Swim Group and the overseas entities).

Lastly, in relation to the balance of convenience, Justice O’Bryan noted that the application was brought on an ex-parte basis to avoid risk of the dissipation of assets. An ex-parte application is a Court proceeding where only the party seeking the Court order appears before the Court. In those circumstances, His Honour ordered that the orders would continue until 12 June 2019, at which time the prospective respondents and associated entities would have an opportunity to be heard. On this basis, it was found that the prejudice to the prospective respondents and associated entities would be temporarily confined. The freezing orders have now been extended until the hearing and determination of the substantive proceedings.

The misleading and deceptive conduct proceedings in the Federal Court

After obtaining the freezing orders the ACCC instituted proceedings in the Federal Court against Jump Swim, alleging that it made false, misleading or deceptive statements about Jump Swim School franchises in contravention of the ACL, as described above. Mr Campbell is also a respondent in the proceedings. The ACCC claims that Mr Campbell was involved in the conduct.

According to the ACCC’s Concise Statement dated 17 June 2019, the ACCC claims that Jump Swim made false or misleading representations in its promotional material about the time it would take to set up an operating swim school business franchise in breach of sections 18 and 29 of the ACL, and that Jump Loops accepted payment from franchisees without providing operational franchises within the time specified or within a reasonable time, and in circumstances where it did not have reasonable grounds to believe it could do so in contravention of section 36 of the ACL.

In a media release dated 18 June 2019 the ACCC says that many franchisees were not provided with an operational swim school within the represented time frame of 12 months or at all. The ACCC Chair Mick Keogh also said “Franchisors need to take their obligations under the Australian Consumer Law seriously. Purchasing a franchise is a big decision, and people looking to open a franchise business rely on the information from the franchisor being accurate…We allege this conduct caused substantial harm to franchisees who paid significant sums but did not receive an operational swim school within the time specified, or at all”.

The ACCC is seeking injunctions, declarations, pecuniary penalties, redress for franchisees, disqualification orders, and orders as to findings of fact, and costs.

What this means for Jump Swim franchisees

Jump Swim franchisees should keep informed of the ACCC’s action as it proceeds, as the outcome may directly affect them. Should there be orders made against Jump Swim or if Jump Swim becomes insolvent, this could have immediate repercussions for them.

Are you a franchisor or franchisee?

These proceedings act as a reminder to all potential franchisees to do their own due diligence before entering into a franchisee agreement and making payment.

Franchisors also need to be very careful about what promises they make to prospective franchisees.

Williams + Hughes can assist you in several ways, including the following:

For further information on how we can assist please contact Leanne Allison or Damian Quail on +61 8 9481 2040 or leanne.allison@whlaw.com.au and damian.quail@whlaw.com.au.

This article is general information only, at the date it is posted. It is not, and should not be relied upon as, legal advice. This article might not be updated over time and therefore may not reflect changes to the law. Please feel free to contact us for legal advice that is specific to your situation.

Employers should take note of changes to the employment landscape that take effect on 1 July 2019.

Increase in the National Minimum Wage and modern award rates

As discussed in a separate Williams + Hughes Insight, from 1 July 2019 the:

Changes to the Maximum Superannuation Contributions Base

The Maximum Superannuation Contributions Base is set by the Federal Government each year. It is used to determine the maximum limit on any individual employee’s earnings base for each quarter for superannuation guarantee payment purposes. An employer does not have to pay the superannuation guarantee for the portion of earnings above this limit.

From 1 July 2019 the Maximum Superannuation Contributions Base increases to $55,270 per quarter, up from $54,030. So, the maximum superannuation guarantee payments that an employer is liable to pay from 1 July 2019 per employee is 9.5% of $55,270, or $5,250.65 per quarter. Calculations should always be made on a quarterly, not annual, basis.

Changes to the High Income Threshold

From 1 July 2019 the high income threshold will increase to $148,700 per annum (from $145,400 per annum). This is important because the high income threshold sets the limit on an employee’s ablity to bring unfair dismissal proceedings. If an employee’s annual rate of earnings is more than the high income threshold, the employee is not able to bring an unfair dismissal claim unless they are covered by a modern award or enterprise agreement.

The increase to the high income threshold also means that the maximum payable compensation for unfair dismissal increases to $74,350, which is 50% of the new high income threshold.

The increase to the high income threshold also sets the minimum guaranteed earnings hurdle for an employee to be a “high income employee” for the purposes of modern award coverage. If a high income guarantee is entered into, the employee is not subject to the application of any modern award.

When calculating earnings for the purpose of the high income threshold, the following items are included:

The following are not included as part of an employee’s earnings:

New whistleblower laws

Under the new whistleblower regime, public companies, proprietary companies that are trustees of a superannuation entity and large proprietary companies must have a compliant whistleblower policy and must provide it to their employees.

As discussed in a separate Williams + Hughes Insight, from 1 July 2019 new asset, revenue and number of employees thresholds apply when determing whether a company is a large proprietary company.

The new whistleblower regime takes effect from 1 July 2019. Although the new regime applies to disclosures made on or after 1 July 2019, the disclosures may relate to conduct that occurred before that date.

The requirement to have a whistleblower policy in place commences on 1 January 2020, although a small proprietary company that becomes a large proprietary company after 1 January 2020 will have an additional six months to establish a whistleblower policy.

Given that companies need to comply with the new laws from 1 July 2019 and must have compliant policies in place by the dates referred to above, companies must take steps to prepare compliant whistleblower policies. Managers and staff must also be trained to properly handle disclosures that are protected under the new whistleblower laws - the new laws require this. The whistleblower policies must also be made available to officers and employees of the company.

Williams + Hughes can assist you in several ways:

For further information on how these changes may impact on your business please contact Damian Quail or Matthew Lenhoff on +61 8 9481 2040 or damian.quail@whlaw.com.au or matthew.lenhoff@whlaw.com.au.

This article is general information only, at the date it is posted. It is not, and should not be relied upon as, legal advice. This article might not be updated over time and therefore may not reflect changes to the law. Please feel free to contact us for legal advice that is specific to your situation.

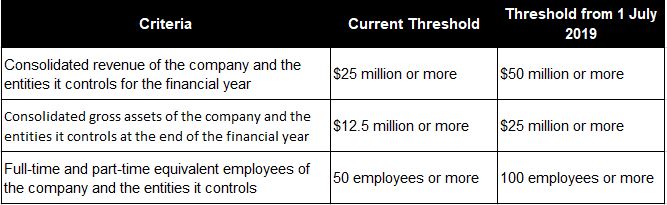

Recent changes to the Corporations Act 2001 remove the need for many companies to lodge annual financial accounts with ASIC.

With effect from 1 July 2019, the criteria in the Corporations Act 2001 for classification as a “large proprietary company” have been changed. The revenue, asset and employee thresholds that determine whether a proprietary company is considered “large” will double.

Why is this important?

Large proprietary companies are required to prepare and lodge an annual financial report, a director’s report and an auditor’s report with ASIC each financial year. This can be both costly and time consuming.

In addition, reports that are lodged with ASIC become publicly available documents - so competitors and customers can easily access sensitive, private financial information about a company.

If a company is required to lodge the required reports but fails to do so, penaltieDamian Quails can be imposed on the company and its officers.

Avoiding the requirement to lodge financial reports with ASIC will not only save a company time, money and effort, but will also keep private financial information confidential. With some exceptions, small proprietary companies generally do not need to comply with these requirements to lodge (but are required to keep sufficient financial records).

So, it pays to be small!

What is the change?

The Corporations Amendment (Proprietary Company Thresholds) Regulations 2019, which will commence on 1 July 2019, amend the definition of “large proprietary company” by doubling the current revenue, assets and employee thresholds. A proprietary company will be “large” if it meets two of the three thresholds at the end of its financial year, as shown in the table below:

The doubling of the thresholds will relieve many proprietary companies from the ASIC reporting obligations. The Federal Government estimates the changes will reduce SME regulatory compliance costs by $81.3 million annually, with a third of proprietary companies currently classified as large expected to fall below the new mandatory reporting thresholds.

What should you do now?

If your company is currently classified as a large proprietary company you should closely consider the revenue, gross assets and employee thresholds to determine whether the company may fall below the increased thresholds from 1 July 2019. If so, your company may be relieved from the time and costs associated with the compliance obligations of a large proprietary company. And you can keep your private financial information out of the hands of your customers and competitors!

For further information on how these changes may impact on your business please contact Damian Quail on +61 8 9481 2040 or damian.quail@whlaw.com.au.

This article is general information only, at the date it is posted. It is not, and should not be relied upon as, legal advice. This article might not be updated over time and therefore may not reflect changes to the law. Please feel free to contact us for legal advice that is specific to your situation.

All employers should be aware of the Fair Work Commission's (FWC's) decision regarding the 2018/2019 annual wage review.

The FWC announced a 3% increase from the first full day period on or after 1 July 2019 to the:

The FWC’s decision is lower than last year’s 3.5% increase to the national minimum wage (and lower than the 3.3% increase from the previous year). The FWC stated that the prevailing economic conditions justified a lower increase this year.

In light of the FWC’s decision, it is important that employers review their rates of pay before 1 July 2019 to ensure employees are appropriately paid in accordance with the new wage rates. There can be significant penalties against employers, and potentially directors, who fail to meet their minimum wage obligations.

For further information on how these changes may impact on your business please contact us on +61 8 9481 2040.

This article is general information only, at the date it is posted. It is not, and should not be relied upon as, legal advice. This article might not be updated over time and therefore may not reflect changes to the law. Please feel free to contact us for legal advice that is specific to your situation.