General Enquiries:office@whlaw.com.au

Perth:+61 8 9481 2040

Geraldton:+61 8 9921 2344

It is not uncommon for businesses to advertise a headline price for goods and services to their customers, and to only disclose optional costs in the fine print or in a manner that is not necessarily clear to customers. This is no longer permitted. Some businessess will need to change their pricing practices, particularly businesses selling goods online.

The Treasury Laws Amendment (Australian Consumer Law Review) Bill 2018 amends the Australian Consumer Law contained within the Competition and Consumer Act 2010, and imposes an obligation on businesses operating in Australia to ensure transparent pricing for consumers. As of 26 October 2019, businesses must display the total price for the goods and services including all pre-selected optional items. In other words, if optional components are pre-selected or automatically applied by the seller, these options must be included in the headline price. The customer then has the option to remove the pre-selected options selected in order to pay a lower price.

These new laws will especially affect businesses who sell goods and services online. The Explanatory Memorandum to the new legislation provides some helpful examples in relation to airlines. For example, if an airline fare is $500 and a website pre-selects an optional carbon offset fee of $5, then the headline price must be $505, not $500. However, if the carbon offset fee is not pre-selected or automatically applied, then the ticket can be advertised at $500.

The same approach is applicable for promotions which display only a portion of the total price. Businesses must ensure that the total price is displayed just as clearly as the fractional price. Essentially, the new laws aim to avoid the situation where headline prices are advertised initially, but once the customer clicks through the website the price is increased to include pre-selected options and charges.

Businesses should ensure that their pricing strategies conform with the new laws.

If you would like further information regarding the new laws please contact Damian Quail.

This article is general information only, at the date it is posted. It is not, and should not be relied upon as, legal advice. This article might not be updated over time and therefore may not reflect changes to the law. Please feel free to contact us for legal advice that is specific to your situation.

The importance of minute taking at Board meetings was recently highlighted by the Financial Services Royal Commission. The Governance Institute of Australia and the Australian Institute of Company Directors have collaborated to publish a Joint Statement of Board Minues (Joint Statement, available on the AICD’s and the Governance Institute's websites), which outlines key principles and best practice approaches to minute taking and document retention.

In many ways, the Joint Statement provides a “best practice” guideline for recording decisions and discussions at Board meetings. Company officeholders would be wise to carefully review the Joint Statement and ensure they are adequately recording minutes of Board meetings and complying with their statutory obligations. We have summarised below five key takeaways from the Joint Statement.

1. Board minutes are a legal record

Board minutes are a legal record of Board decisions. The minutes may be the best, and sometimes only, evidence of the decision making process at Board meetings. Minutes may help to establish that directors have satisfactorily exercised their powers and discharged their duties.

Minutes should include the key points of discussion and detail the issues and risks the Board has considered. If judgment is required and directors are balancing a number of competing risks, it is prudent to consider whether the minutes capture them adequately. This is important where directors wish to rely on the “business judgement rule”.

2. Balance the level of detail

The Joint Statement highlights the importance of ensuring the information recorded contains a sufficient level of detail. Too much information can be unhelpful and too little can cause ambiguity. The right balance needs to be struck.

In summary, Board minutes should record:

However, Board minutes should not record:

The Board paper and supporting documentation used in the decision making process should influence the details in the minutes. Where appropriate, minutes should refer to the Board paper and supporting documents, but avoid repeating the contents. In that regard, directors should take an active role in reviewing Board papers and satisfying themselves that they provide adequate information on which to base decisions.

3. Stick to a particular style

The Joint Statement provides some helpful stylistic tips for drafting minutes, including that minutes should:

4. Consider regulatory and statutory compliance

It is a requirement of the Corporations Act 2001 that a company keep a minutes book in which proceedings and decisions at Board meetings are recorded within one month of the meeting. It is important directors understand the statutory obligation - failing to do so is an offence of strict liability.

Minutes must be signed by the chair of the meeting, or by the chair of the next meeting, within a reasonable time after the meeting takes place. All directors should be given an opportunity to review and discuss the minutes before they are approved and signed.

Companies should implement (or review their current) document retention policies. It may be necessary to seek legal advice regarding what policies should be implemented and the obligations to safeguard evidence.

5. Be wary of Legal Professional Privilege

It is common for Boards to consider legal advice. A cautionary approach should be taken in determining the degree of privileged information to include in the minutes. In many cases, it may be sufficient to document that the Board considered relevant legal advice when making a particular decision. Any privileged information in the minutes should be clearly identified and ideally be included in an appendix. Importantly, where minutes refer to privileged advice they should not be provided to third parties without first obtaining legal advice as this may waive privilege.

If you require further advice about conducting Board meetings or corporate governance or advice generally, please do not hesitate to contact Cassandra Bailey at cassandra.bailey@whlaw.com.au or 9481 2040.

This article is general information only, at the date it is posted. It is not, and should not be relied upon as, legal advice. This article might not be updated over time and therefore may not reflect changes to the law. Please feel free to contact us for legal advice that is specific to your situation.

The interaction between section 249D and section 203D of the Corporations Act 2001.

There has been a significant rise in shareholder activism over the last couple of years. Often this is driven by shareholders with financial capacity and vision for the company, wanting to turn around the company’s stagnant fortunes and share price. A common mechanism for shareholders to replace the board of a public company is a section 249D notice under the Corporations Act 2001. A section 249D notice allows a shareholder or shareholders with at least 5% of a company’s share capital to force the company to call a general meeting to vote on resolutions proposed in the notice.

There are a number of formal requirements, and many tricks and traps for shareholders, in utilising the section 249D notice provisions.

The section 249D notice must be in writing, state any resolution to be proposed at the meeting, be signed by the members making the request, and be given to the company.

On receipt by the company of a valid section 249D notice:

If the section 249D notice proposes resolutions for the removal of all or certain directors, the requirements of section 203D Corporations Act 2001 also need to be kept in mind. Section 203D(2) requires shareholders who want to remove a director at a general meeting, to give notice of their intention at least 2 months before the meeting is to be held. The second part of section 203D(2) provides that if the company calls a meeting after that notice of intention is given, the director can be removed at the meeting even if the meeting is held less than 2 months after the notice of intention is given.

It is the structure of section 203D and the interplay between sections 203D and 249D that tends to cause grief for requisitioning shareholders.

Common mistakes

Because section 249D does not explicitly refer to section 203D it is sometimes overlooked. If a section 203D notice has not been given, or it is given after the section 249D notice, a proposed resolution in the section 249D notice to remove a director is ineffective and there would be a question whether the company had to call the meeting at all.

Other issues we sometimes see are the two notices being combined into one, or being issued on the same day.

The two notices cannot be combined. That is, the section 249D notice cannot also serve as the shareholder giving notice of their intention under section 203D. There are at least a couple of reasons for this.

As well as being separate notices, the section 203D notice should be given to the company before the section 249D notice is delivered; not on the same day. That is the only way sections 203D and 249D can operate harmoniously and with full effect.

The section 203D notice can and should be given in such a way that it is possible for the meeting to be held after the 2 month period required by section 203D (although the company may then make its own decision to bring the meeting forward as foreshadowed by the second part of section 203D). This can only happen if the section 249D notice is given to the company at least a day after the section 203D notice is given; preferably longer (out of an abundance of caution). The exact timing will depend on the circumstances in each case.

We recommend that shareholders intending to use section 249D to remove directors from the board of a public company get legal advice on the process, and assistance to ensure each step is properly planned and executed. Conversely, directors receiving such notices should seek prompt advice about how to manage their obligations under the Corporations Act 2001 and what steps can be taken to defend themselves and the company against the attack.

For advice to prepare for or defend an attempted board spill, please contact Dominique Engelter on +61 9481 2040 or dominique.engelter@whlaw.com.au.

This article is general information only, at the date it is posted. It is not, and should not be relied upon as, legal advice. This article might not be updated over time and therefore may not reflect changes to the law. Please feel free to contact us for legal advice that is specific to your situation.

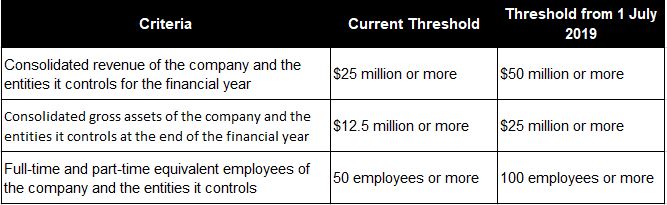

Recent changes to the Corporations Act 2001 remove the need for many companies to lodge annual financial accounts with ASIC.

With effect from 1 July 2019, the criteria in the Corporations Act 2001 for classification as a “large proprietary company” have been changed. The revenue, asset and employee thresholds that determine whether a proprietary company is considered “large” will double.

Why is this important?

Large proprietary companies are required to prepare and lodge an annual financial report, a director’s report and an auditor’s report with ASIC each financial year. This can be both costly and time consuming.

In addition, reports that are lodged with ASIC become publicly available documents - so competitors and customers can easily access sensitive, private financial information about a company.

If a company is required to lodge the required reports but fails to do so, penaltieDamian Quails can be imposed on the company and its officers.

Avoiding the requirement to lodge financial reports with ASIC will not only save a company time, money and effort, but will also keep private financial information confidential. With some exceptions, small proprietary companies generally do not need to comply with these requirements to lodge (but are required to keep sufficient financial records).

So, it pays to be small!

What is the change?

The Corporations Amendment (Proprietary Company Thresholds) Regulations 2019, which will commence on 1 July 2019, amend the definition of “large proprietary company” by doubling the current revenue, assets and employee thresholds. A proprietary company will be “large” if it meets two of the three thresholds at the end of its financial year, as shown in the table below:

The doubling of the thresholds will relieve many proprietary companies from the ASIC reporting obligations. The Federal Government estimates the changes will reduce SME regulatory compliance costs by $81.3 million annually, with a third of proprietary companies currently classified as large expected to fall below the new mandatory reporting thresholds.

What should you do now?

If your company is currently classified as a large proprietary company you should closely consider the revenue, gross assets and employee thresholds to determine whether the company may fall below the increased thresholds from 1 July 2019. If so, your company may be relieved from the time and costs associated with the compliance obligations of a large proprietary company. And you can keep your private financial information out of the hands of your customers and competitors!

For further information on how these changes may impact on your business please contact Damian Quail on +61 8 9481 2040 or damian.quail@whlaw.com.au.

This article is general information only, at the date it is posted. It is not, and should not be relied upon as, legal advice. This article might not be updated over time and therefore may not reflect changes to the law. Please feel free to contact us for legal advice that is specific to your situation.

Recent amendments to the Competition and Consumer Regulations 2010 impose new mandatory wording requirements in relation to the supply of services and also the supply of goods in combination with services.

The new requirements take effect on 9 June 2019. Failure to comply with the new laws can attract a $50,000 fine.

Australian businesses that have not updated their trading terms and conditions, product manuals, warranty cards, marketing materials, product packaging and websites must act quickly to avoid breaching the new laws.

The new mandatory wording requirements make it compulsory for businesses to inform consumers that any warranties or guarantees against defects that are contained in a business’ documents or website do not override the statutory consumer guarantees provided in the Australian Consumer Law (the ACL).

The new requirements apply in respect of any services supplied at a value of $40,000 or less or in respect of any services of a kind that are usually acquired for personal, domestic, or household use or consumption.

The new laws prescribe mandatory text that must be reproduced verbatim. The specific wording required depends on whether the warranty or guarantee against defects applies in relation to the supply of services or the supply of goods in combination with services. The supply of goods alone is already covered by mandatory text requirements that have been part of the ACL for some time.

The ACL also imposes other requirement that warranty documentation and T&C’s must comply with. Now is a good time to ensure your documents and websites are up to date.

For further information on how these changes may impact on your business please contact Damian Quail, Director at Williams + Hughes on +61 8 9481 2040 or damian.quail@whlaw.com.au.

This article is general information only, at the date it is posted. It is not, and should not be relied upon as, legal advice. This article might not be updated over time and therefore may not reflect changes to the law. Please feel free to contact us for legal advice that is specific to your situation.

Williams + Hughes advise public and private companies and individuals across a wide spectrum of industries. Our range of commercial litigation expertise and experience, coupled with ready access to senior legal personnel and our responsiveness, makes us top choice commercial litigation lawyers in Western Australia.

We recognise that clients often choose their legal advisors based on their knowledge and understanding of the client’s industry. Our lawyers work hard to understand the commercial and technical drivers underpinning our clients’ industries, as this enables us to quickly and efficiently advise on complex and technical matters affecting their businesses.

Get in touch with our top tier commercial litigation lawyers in Perth or Geraldon to see how we can assist you.

We have significant experience providing the full spectrum of advice required in relation to major resources, exploration and mining projects. We have advised in relation to many projects in the Goldfields, Pilbara and Mid West and overseas, particularly in relation to acquisitions and divestments, joint ventures, farm-ins, plant and equipment hire and supply, contract mining, mining services and underground and directional drilling.

Our expertise in this area includes:

We have specialist expertise in gold, base metals and mineral sands projects.

Our notable and significant transactions include:

LLB, B.Com (Acc & Fin) (Hons) MAICD

Damian is a Director and Principal of Williams + Hughes. He has practiced as a lawyer for over 28 years in the commercial, resources, agribusiness, software and technology fields. He has managed many large deals, including major investments, farm-ins and JV’s, asset and share sale deals, capital raising transactions and construction matters.

Damian acts for a wide range of clients, including ASX and TSX listed companies, large private family groups and small to medium enterprises. Damian has special expertise in M&A transactions.

Damian adopts a pragmatic approach with a strong focus on ensuring his advice adds value and allows clients to get deals done.

Damian has significant business experience outside of law. This experience helps ensure he does not waste time on legal points that are not commercially important. His past and current roles include:

Damian is a current member of the Australian Institute of Company Directors, Energy and Resources Law and the Law Society of Western Australia.

Damian is based in our West Perth office. He is a regular legal CPD seminar presenter for the Law Society of Western Australia and Legalwise, where he has presented extensively on M&A topics. He is married with three children and enjoys making TV shows, travelling and playing indoor cricket.

Some of the significant matters Damian has advised on include:

Mining, resources and mining services

Mergers & Aquisitions

Pipelines, Tanks and Terminals

Construction

Software and IT related